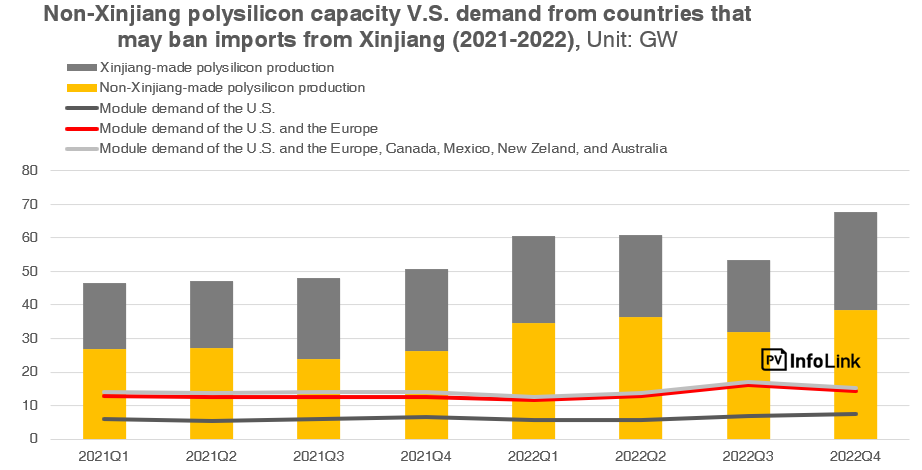

The production capacity of polysilicon used in ingot production in 2021 is 710,000 tons all over the world. 610,000 tons of this capacity is produced in China. Three big companies based in Germany, Norway and America meet this remaining production outside of China. The trade agreement signed in 2020 between China, which holds the market, and the USA, facilitated the commercial lives of these three manufacturers by enabling them to sell to the Chinese market on favorable terms. About half of China's polysilicon production takes place in the Xinjiang Autonomous Region. The working conditions of the workers in this region are a matter of debate in the West, and serious restrictions may be imposed on imports from this region. However, these obstructions could exacerbate the trade war between China and the United States, putting three major polysilicon producers in the West in a difficult position again.

In the photovoltaic industry, polysilicon is used in the production of ingots. Since the majority of ingot production is done in Mainland China, polysilicon manufacturers need this region as a market. However, the restriction imposed by China on the export of non-value-added raw materials leads to the export of polysilicon produced in China as wafer and its continuation products. Therefore, this situation strengthens the desire for commercial cooperation between polysilicon manufacturers and companies producing ingots outside of Mainland China. During purchasing operations; It is necessary to analyze the supply-demand relationship, the reasons and power of the demand between the seller and the buyer, the future meaning of trade. If these issues are not fully understood, the operation cannot be carried out properly and good results cannot be obtained.

Capacity for the global polysilicon market is currently advancing at 50 gw. With the addition of new production lines, this capacity will approach 70 gw by the end of 2022. In other words, a capacity increase of about 30% is expected. However, as I mentioned in my previous articles, the production targets announced by the panel manufacturers are in the direction of a two-fold increase. In this situation, it is expected that until the end of 2022, the supply-demand balance will be positioned on the supply shortage side.

While we expect the upward trend of Chinese polysilicon price currently above 30 usd/kg to continue, some easing in early 2022 is possible, but it seems difficult to regress to prices below 20 usd/kg last year. The sales policy of manufacturers outside the mainland of China, on the other hand, will proceed a few dollars below these prices, with the foresight of logistics costs, as has been the case so far. The current situation of the global market will be changed by the increase in polysilicon demand with ingot production facilities to be established in the West.

- Log in to post comments